Industry News

After the industrial contradiction is resolved, the valuation level of the steel industry is expected to be restored

Iron and steel enterprises in environmental protection, high-end, asset structure and other aspects have formed obvious differentiation, through the standard guidance and other market-oriented means, survival of the fittest, can optimize the industry supply pattern, to achieve industry quality upgrading.

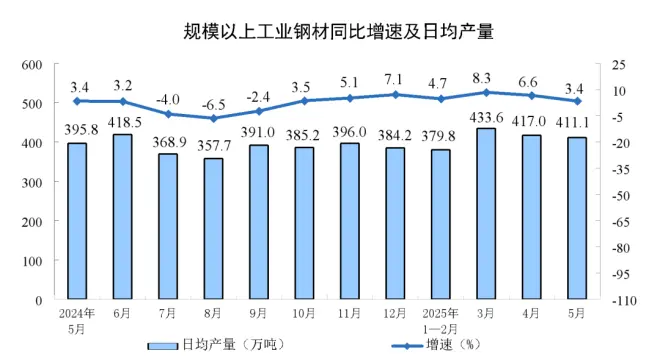

1. The steelindustry is an important basic industry in China. Since 2022, with the gradual decline in real estate demand, the structure of China's Steel demand has gradually changed from building owners to manufacturing. In the face of changes in the downstream demand structure of steel, the supply structure has not changed in time, and the market supply has remained high, resulting in a continuous decline in the industry's prosperity and serious losses in the industry, which in turn has led to the lack of continuous research and development capabilities in the industry, which cannot provide sufficient guarantee for the high-end development of the manufacturing industry in the medium and long term. Therefore, under the current situation of total demand and structural changes, the industry needs to reduce inefficient production capacity and improve the prosperity of the industry, so as to provide strong material support for the long-term development of the manufacturing industry.

2. Although the steel industry is facing the contradiction between supply and demand at this stage, and the overall profit of the industry is declining, with the in-depth promotion of a series of "steady growth" policies, the total demand for steel is expected to remain stable or even slightly increased marginally under the support of real estate bottoming out, infrastructure investment, sustainable development of manufacturing industry, and high steel exports. At the same time, under the macro trend of high-quality economic development and new quality productivity, especially high-end Steel Products that benefit from the energy cycle, domestic substitution, and high-end equipment manufacturing are expected to fully benefit. Overall, the future of the steel industry industry pattern is expected to be stable and better, superimposed on the current part of the company has been in the undervalued area, at this stage there are still structural investment opportunities, especially with a high level of gross profit margin of excellent special steel enterprises and cost control, with scale effect of the leading steel enterprises, there are opportunities for valuation repair in the future.

3. Special steel is a policy to strongly support the industry, China's high-end special steel new materials have "import substitution", outside the "global share increase", the current proportion of high-end special steel in China is about 4%, and Japan, Europe and the United States and other developed countries are still quite different, China's high-end manufacturing industry is developing rapidly, high-end special steel demand is expected to usher in rapid growth, high-end special steel enterprise valuation is expected to increase, from the perspective of the valuation of special Steel Companies in developed countries, mostly at the level of 15-25 times, Japan, The rapid development stage of special steel in Europe and the United States has passed, while China's high-end special steel is still in the growth period, and the application of new energy, shipbuilding, and aerospace industries is in a period of vigorous development, and should enjoy a certain valuation premium.